What are they?

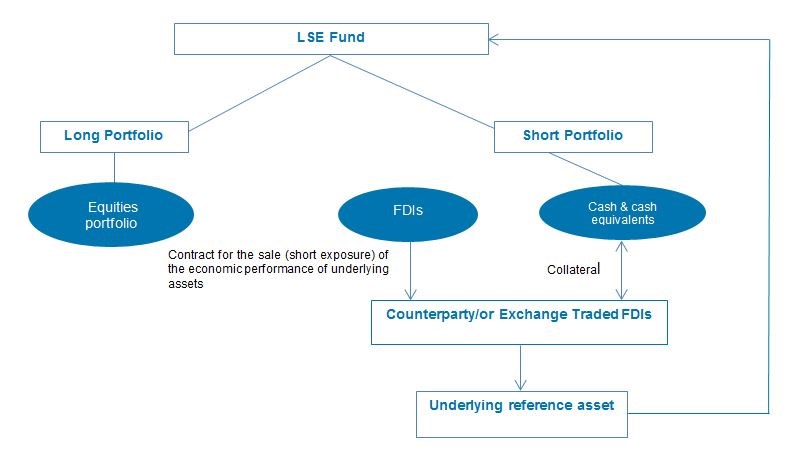

UCITS Long-Short Equity Funds (LSE Funds) are UCITS funds that seek to generate capital appreciation whilst minimising the impact of market volatility by taking both long and short exposure to equities. As illustrated in the diagram below, LSE Funds are constructed by buying a portfolio of equities (ie “long” portfolio) that the investment manager anticipates will appreciate in value over time. At the same time, the LSE Fund takes short exposure to equities by investing in financial derivative instruments (FDI) on equities (ie “short” portfolio) that are anticipated to fall in value over time. The short portfolio is comprised of a combination of cash/liquid instruments and FDIs which take short economic exposure to underlying assets such as individual equities, equity indices, or baskets of equity securities. The cash/liquid portfolio is used as cover or collateral for the short positions of the LSE Fund. LSE Funds use FDIs, typically forwards/futures, swaps, options, or contracts for difference, for the purpose of taking short exposure to returns linked to the performance of equities. If the equities fall in value, the LSE Fund will generate investment returns.

Shouldn’t UCITS LSE Funds be established as alternative investment funds (AIFs)?

Typically, funds adopting a long-short investment strategy are categorised as AIFs under the Alternative Investment Fund Managers Directive 2011/61/EU. However, in recent years legislative developments have increased the range of eligible assets that UCITS may acquire and also have expanded the type of investment strategies that UCITS can implement. This has led to significant growth of so-called alternative UCITS or absolute return UCITS, which LSE Funds are part of.

What type of investors are LSE Funds aimed at?

LSE Funds have broad investor appeal. However, as the UCITS regime is acknowledged as a respected regulatory framework, LSE Funds are also popular with institutional investors, particularly in the EU. The growth of alternative UCITS and their marketability has enabled traditional hedge fund managers to evolve their business strategies and redefine their target client base, and in particular to design funds that cater for the requirements of institutional and high net worth investors.

Synthetic prime brokerage products

LSE Funds are not permitted under UCITS regulations to appoint a prime broker that lends to the LSE Fund for investment purposes. Furthermore, LSE Funds cannot borrow stocks in order to take short positions and may only take short exposure by investing in FDIs. At first glance, this would appear to prevent prime brokers from providing prime brokerage services to the UCITS. However, the prime brokerage industry has devised “synthetic prime brokerage” products, which allow LSE Funds to invest in FDIs as a substitute for borrowing equities in order to achieve short positions and to achieve leverage by providing margin financing in relation to FDIs such as forwards, futures or swaps that provide a leverage exposure for the LSE Fund’s portfolio. The use of FDIs permits the LSE Fund to achieve both long and short exposures, however, the Central Bank requirements, summarised below, apply to such strategies.

Central Bank requirements for the use of FDI for investment purposes

The use of FDI for investment purposes is fundamental to the investment strategies of LSE Funds. Like all UCITS that invest in FDIs, LSE Funds must comply with the following requirements:

(i) Investment in FDIs must only give an LSE Fund exposure to assets that the LSE Fund is permitted to invest in directly, in accordance with its prospectus and constitutional document. Accordingly, the underlying assets of LSE Funds must be comprised of the following:

-

UCITS eligible asset (ie transferable securities, money market instruments, units in collective investment schemes, deposits with credit institutions, FDI that meet the requirements of the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations 2011 (UCITS Regulations) and the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1)) (Undertakings for Collective Investment in Transferable Securities) Regulations 2015 (CBI UCITS Regulations), including FDI having one or several characteristics of those assets

-

Financial indices

-

Interest rates

-

Foreign exchange rates

-

Currencies

(ii) The FDIs do not expose the LSE Fund to risks which it could not otherwise assume (e.g. gain exposure to an instrument or issuer which the UCITS cannot have a direct exposure);

(iii) The FDIs do not cause the LSE Fund to diverge from its investment objectives disclosed in its prospectus;

(iv) The FDI is:

-

Dealt on a regulated market

-

Transacted with a counterparty who is an eligible credit institution

-

Transacted with an investment firm authorised in accordance with the Markets in Financial Instruments Directive 2014/65/EU, which complies with the credit rating requirements

-

Transacted with a group company of an entity that:

-

Complies with the Credit Rating Requirements, and

-

Is approved as a bank holding company by the Federal Reserve of the United States of America where that group company is subject to bank holding company consolidated supervision by the Federal Reserve of the United States of America

-

If such an FDI is subject to a novation then the new counterparty must satisfy one of the criteria listed above or the FDI must be transacted with a central counterparty that is authorised or recognised under EU Regulation No. 648/2012 on OTC Derivatives, Central Counterparties and Trade Repositories (EMIR) or a third country entity recognised by ESMA pursuant to Article 25 of EMIR; for example, ESMA confirmed that LCH Limited, ICE Clear Europe Limited and LME Clear Limited will receive such recognition post-Brexit.

Issuer Concentration limits

Like all UCITS, LSE Funds are required to comply with risk spreading rules (or issuer concentration limits) which limit the investment that may be made in a single issuer to 10% of the LSE Fund’s net assets. The issuer concentration limits should be complied with if securities are held directly by the LSE Funds and also when exposure to an issuer is taken through the holding of FDIs. In the case of FDIs, the LSE Fund is required to assess its exposure to an underlying issuer by using the commitment approach whereby the economic exposure of each FDI is converted into the market value of an equivalent position in the underlying security by using the methodology prescribed in the UCITS regulations.

Counterparty exposure limits

LSE Funds are required to limit their exposure to any single counterparty to 5% of its net asset value. This can be extended to 10% where the counterparty falls within the category of certain credit institutions. In assessing risk exposure to a counterparty, an LSE Fund:

-

Must calculate exposure to the counterparty using the positive mark-to-market value of the FDI entered into with the counterparty

-

May enter into legally enforceable netting arrangements in respect of over-the-counter (OTC) FDI with the same counterparty (ie offsetting losses in one investment through gains made in other investments) but not in relation to any other exposures held with that same counterparty, and

-

May receive collateral in order to reduce exposure to the FDI counterparty provided such collateral complies with certain eligibility requirements

Cover Requirements for FDI Positions

An LSE Fund is required to have either cash or securities to settle the obligations it owes under an FDI contract. Where the FDI is settled in cash, the LSE Fund must hold liquid assets (ie cash or money market instruments) as “cover” to ensure that it can pay for the position it held in the FDI. Where physical delivery of the underlying asset is required for settlement, the LSE Fund must hold the underlying asset, or sufficiently liquid assets where the underlying asset consists of highly liquid fixed income securities and/or the LSE Fund considers that the exposure can be adequately covered without holding the underlying asset and details are disclosed in the prospectus or, where applicable, supplement of the LSE Fund.

Risk Management Process and Risk Measurement

Like all UCITS that invest in FDIs, LSE Funds are required to implement a detailed risk management process (RMP) that sets out how the LSE Fund will monitor and manage risk relating to the use of FDIs. An LSE Fund may apply either the “Commitment Approach” or alternatively use an alternative risk measurement methodology such as the Value-at-Risk model (VaR). Typically, LSE Funds using high levels of leverage use the VaR model. The VaR model allows for a greater degree of leverage; for example, it would not be unusual for an LSE Fund to have a gross exposure that exceeds 500% of its net asset value.

Calculation of global exposure using the VaR approach must be carried out in accordance with Schedule 4 of the CBI UCITS Regulations. The following additional requirements also apply in such circumstances:

-

Back testing of the VaR model is required to be carried out on, at least, a monthly basis (ie a formal statistical process to compare actual portfolio returns to the VaR predicted)

-

Regular stress tests must be regularly be carried out, at least monthly, on all risks that affect the value or the fluctuations of the LSE Fund to any significant degree in accordance with the written stress test policy of the LSE Fund

-

Leverage must be regularly monitored, and

-

The risk profile and investment strategy, together with other risk measurement methods, must be taken into account

Conclusion

LSE Funds have grown to become an established strategy within the UCITS regime. We are continuing to see interest in the formation of alternatives types of UCITS, including LSE Funds, from alternative managers who are seeking to avail of the commercial opportunities that the UCITS brand presents and from more traditional managers who would like to expand the investment products they can offer to investors.

If you have any questions in relation to these matters, please contact a member of our Investment Funds team.

The content of this article is provided for information purposes only and does not constitute legal or other advice.